Lawtitude

Energy Wars and Corporate Markets: The Business Fallout of the Middle East Conflict

For much of the past decade, global markets had grown comfortable with the idea that energy shocks belonged to another era — relics of the oil crises of the 1970s or the geopolitical turmoil that once sent crude prices spiralling overnight. But the renewed tensions across the Middle East have shattered that complacency, reminding corporations and investors alike that energy markets remain inseparable from geopolitics.

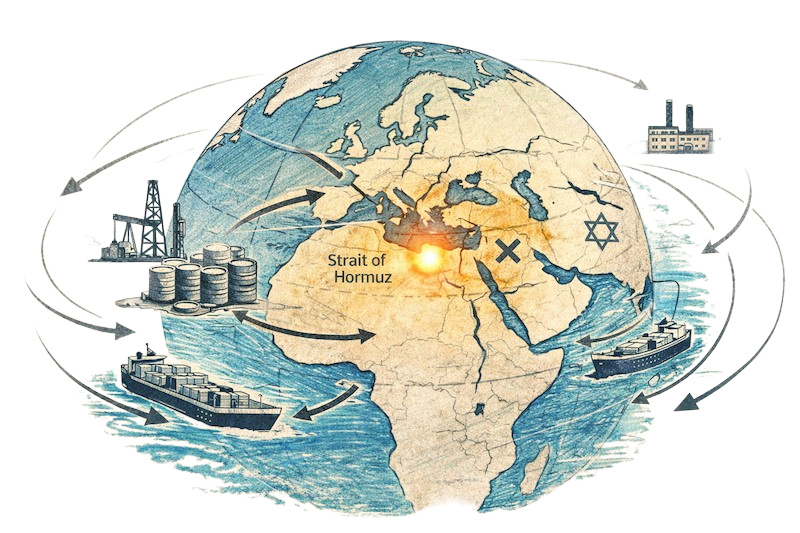

The Middle East still sits at the heart of the world’s energy system. Nearly a third of global oil supply originates from the region, and critical maritime arteries such as the Strait of Hormuz and the Red Sea shipping routes carry vast quantities of oil and liquefied natural gas to markets in Asia, Europe and beyond. When conflict flares in this region, it does not remain a regional event. It becomes a global economic story.

What has emerged in recent months is not simply a military confrontation but an energy market tremor with profound corporate implications.

Markets on Edge

Energy markets react to uncertainty as much as to actual disruption. Even the possibility that conflict might threaten shipping lanes or energy infrastructure can send prices surging. Insurance premiums for vessels travelling through contested waters rise overnight. Freight rates spike. Corporations that depend on steady energy inputs — from manufacturing conglomerates to airlines — suddenly find their cost forecasts thrown into disarray.

For global corporations, the ripple effects begin almost immediately. Oil price volatility translates into higher operating costs, while rising energy prices feed inflation across supply chains. Chemical manufacturers, logistics companies, aviation firms and energy-intensive industries feel the impact first, but the shock eventually travels across sectors.

A rise of even a few dollars per barrel can alter quarterly earnings projections for multinational companies. For firms operating on thin margins, these shifts can determine whether a financial quarter ends in profit or disappointment.

The Supply Chain Domino Effect

The modern global economy depends on an intricate web of supply chains, many of which intersect with Middle Eastern shipping routes. Disruptions to these corridors force shipping companies to reroute vessels, often adding thousands of nautical miles to journeys.

The result is not merely delay but cost — a cost that reverberates through the global economy.

Companies importing raw materials see longer delivery times. Exporters face rising freight bills. Manufacturers must hold larger inventories to guard against uncertainty. What begins as a geopolitical conflict gradually manifests as a logistical challenge for corporate operations across continents.

In boardrooms from Mumbai to Frankfurt, supply chain risk has become a central agenda item once again.

The Return of Energy Hedging

Corporate treasuries are responding in familiar ways. Energy hedging — once considered a technical exercise handled quietly by finance teams — is returning to prominence. Companies are locking in future energy prices through derivatives and long-term supply contracts in an attempt to shield themselves from volatility.

Airlines, among the most energy-sensitive industries, have historically relied on hedging strategies to stabilize fuel costs. But today, even sectors traditionally less exposed to energy price swings are revisiting similar mechanisms.

At the same time, energy producers themselves are navigating a delicate balance. Higher prices boost revenues, but extreme volatility risks destabilizing demand and inviting regulatory intervention. The corporate energy sector thus finds itself in a paradox: benefiting from instability while seeking to avoid its most severe consequences.

A New Era of Corporate Geopolitics

Perhaps the most striking consequence of the crisis is the way it has drawn corporations directly into the orbit of global politics. For decades, multinational companies operated under the assumption that geopolitical risk was largely the domain of governments and diplomats. Today that boundary has blurred.

Energy markets sit at the intersection of politics, security and commerce. When tensions escalate in the Middle East, corporate strategy must adapt in real time — adjusting procurement strategies, revising shipping routes, and recalibrating financial forecasts.

For corporate leaders, the lesson is unmistakable: geopolitics is no longer a distant concern but a boardroom priority.

The Road Ahead

Energy markets have always been shaped by forces beyond economics — wars, alliances, and strategic rivalries. The current conflict in the Middle East is a reminder that the stability of global commerce remains deeply intertwined with the stability of energy supply.

For corporations navigating this landscape, resilience will depend on diversification, risk management and a willingness to adapt quickly to geopolitical change.

In an interconnected global economy, a conflict thousands of miles away can reshape balance sheets, supply chains and investment strategies. The energy wars of today may not always erupt in oil fields or shipping lanes, but their consequences are increasingly felt in corporate boardrooms around the world.